{kind=link}

Interest rates are on rise again. And while it encourages the investors who seek out a fixed income option to invest, these high rates demoralize the new borrowers to take loans.

Of Course this is the intention of the central bank behind raising rates, and people may like to postpone their borrowing for a few years.

However, these high rates are a burden on existing borrowers.As with every rate hike, the floating loan rates will be revised higher, which will further increase the EMI burden.

So, if and when you have some surplus money available, and you seek out a fixed income investment option, it is better to evaluate the same with prepayment of loans you are serving.

Please Understand, 9% earning interest or 9% saving of Interest outgo results the same. But in practice deposit rates are generally lower than borrowing rates.

Until last year, banks were offering mouth watering rates, and with the property market showing the growth signs, and incomes were also stable, many people went for loans.

I recently met a doctor couple who were in their early 40s, and they had almost all kinds of loans in their kitty. Car Loan (they Both have personal cars), Home Loan (Like many others, they found the deal attractive last year), Personal Loan( for home renovation) , Consumer Loan (for new TV, washing machine)

It may sound like a rare case, but believe me in today’s kind of consumerism era these kinds of people are quite normal to find.

Even for your financial goals, you bet on your future income, else Loan options are always there. (Read: Financial Goals of Doctors?)

But this may not go well with your financial future as high borrowing is not a good financial habit.

Now, when this doctor couple’s kids’ school has raised the fee structure, along with the recent Interest rate hikes that have increased the EMI payment, they started feeling the heat and found difficulty in cash flow management. And this is where they decided to seek professional help.

I asked for their financial details as in their Total Income, expenses, assets and liabilities. Plus the goals they target

But I wanted them to repay loans right away with the fixed deposits they are having. And reasons were very clear as Long term investments may generate better returns in future, but that will not ease the pain they are feeling today.

Plus the role of money should always be to make your life easy and simple , not complicated. You can plan for the future well only when your present is comfortable. The problem was with Loans so we will tackle them first and later look at the Investments with the EMIs that have been saved. And at that time we will talk about Budgeting and Cash flow management too.

Factors to consider before prepayment of loans?

The following are some factors to consider when reducing debt exposure.

1. Type of loan:

The first factor you must consider when deciding the prepayment of loans and which loan to close first is the loan type and its impact on your overall finances.

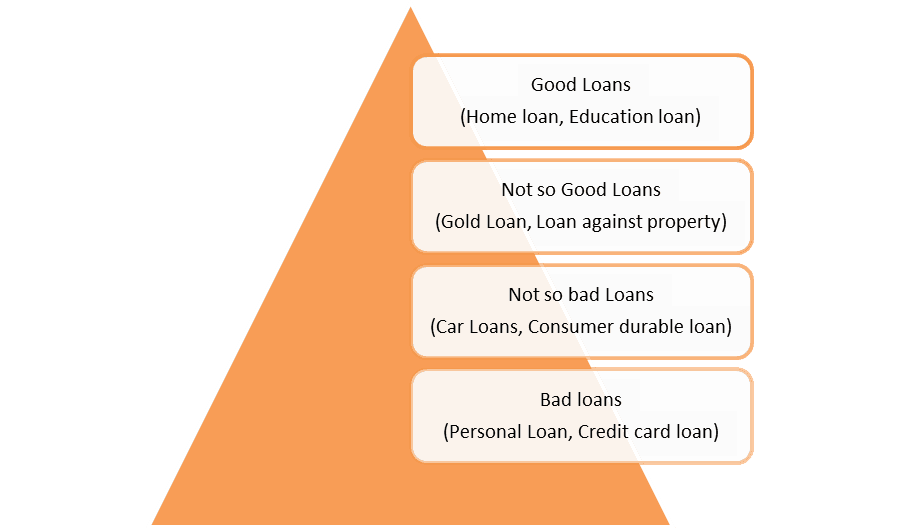

There are two types of loans based on their productivity in your personal finances – Good Loans and Bad Loans.

Bad loans are those taken for personal consumption only. They generally fall under the unsecured category, i.e. no collateral is required and no guarantors are required. The amount of the loan is solely determined by your earning potential and your ability to repay it. For example Personal Loan, Credit card Loan.

In the case of good loans, some productive assets are created, such as homes, intellectual capital, etc. Home loans and Education loans come under this category.

In addition to “good” loans, there are “not so good loans” that are taken on collateral with a specific purpose such as expanding a business or facing an emergency, for example Loan against property or gold loans.

A fourth category is “Not so bad loans”, which result in assets being created, but they are unproductive and depreciable, like Vehicle loans.

You must start with bad loans first, as bad loans do not generate any assets, but are also considered negative by credit scoring agencies. One needs to stay off bad loans as much as possible.

(Also read: Good Loans vs Bad loans)

2. Interest rates and Tenure of Loan

It is common for people to prepay loans that are close to completion, or which have high EMIs. Their focus is on the expense part of the equation rather than the interest outgo.

In an EMI, the interest portion represents the cost of the loan. Therefore, you should understand what savings you can expect from prepaying the loan.

Bad loans can have interest rates as high as 16%-36%. Therefore, it makes sense to close these loans first. However, the tenure of loans also plays an important role in pre-closing decisions.

(Read: All about External Benchmarking of interest rates and its impact on home and car loan)

Let’s understand this with an example of this doctor couple.

In addition to their multiple loans, they took out two at the same time- a personal loan and a car loan.

Personal Loan (5 lakh) – Tenure 5 years, Interest rate 14%, EMI = Rs 11634/-.

Car Loan (7 lakh) – Tenure 7 years, Interest rate 10%, EMI = Rs 11621/-

| Year | Interest outgo (PL) | Interest outgo (CL) |

| 1 | 65355 | 66727 |

| 2 | 54265 | 59111 |

| 3 | 41520 | 50699 |

| 4 | 26871 | 41405 |

| 5 | 10034 | 31138 |

| 6 | 19796 | |

| 7 | 7266 |

This calculation is for illustration purpose only, real rates may vary.

As can be seen from the above calculation, if one has to close either of the loans, they should work on the car loan first, since it will result in more interest savings.

3. EMI outgo :

EMI has an impact on your cash flow. High EMIs mean fewer surpluses to save. A loan is not just a financial burden, but also a psychological one. By getting rid of high EMI loans, you usually gain confidence in your finances. It is therefore better to close those loans first if your high EMIs make you sleepless at night. Although it may not make financial sense, living a stress-free life is priceless.

4. Tax benefits:

Tax benefits indirectly reduce cash outflows. Consider these tax benefits before deciding which loan to prepay first if you have such loans in your portfolio.

With Fixed deposits giving 7.50% taxable and Loans asking 9% with no tax benefit, it is no brainer that one should withdraw the FDs and close the loan. Still, in many cases Investors are so attached to their Savings , especially when they are comfortable paying the EMIs, without realizing that Contining with both does not make financial sense.

And it is amusing when such investors tries to find the High Return generating Investment for their future.

There are many basic things in financial management which requires your attention and fixing those small things sometimes result big and makes a way towards your financial wellness.

Even if you are confident in your Income generating capacity, still making arrangements for Uncertainties is a Practical approach. Because Life has its own Plans.

In times of rising housing costs and rising education costs, sometimes,one cannot avoid taking out loans. It is worse to take out loans for unnecessary consumer durable or for personal consumption.

You should consider your future goals when taking out a loan. In order to make your present perfect, you should not make your future tense.

Take good loans if at all required, service your loan EMIs on time, and avoid loans for consumption or desire.

Thank you for taking the time to read this article.

Can you think of any other factor that I may have overlooked, towards consideration on loan prepayment?