A prospective doctor client approached us for his Investment portfolio review. Of course we could not review the portfolio without having a Financial Plan in place as we have to have a reason attached to all the investments and see if those suit the risk appetite or not.

But his portfolio was different, as he was having only Fixed income products in the same and still wanted us to have a look. Clearly he was a conservative investor and Safety of capital was his prime concern and thus 100% Fixed Income Portfolio.

Since he was not familiar with how mutual funds operate, he mistook these funds for only investing in stocks. The equity risk wasn’t something he was interested in, so he didn’t bother to look into it. The only investments he had were bank savings accounts, PPFs, and other small saving schemes.

However, when FD interest rates dropped to nearly 5% in 2021, he began investing in Debt Mutual Funds on the advice of a friend. Compared to the then FD rates, past returns in debt funds were quite attractive.

Initially, it was an “OK” return, but after the interest rate cycle reversed in the last few months, because bond prices are inversely related to interest rates, his debt mutual fund portfolio returned dropped to nearly 3%.

Currently, he claims debt mutual funds were a mistake, and bank FDs were better. Of Course seeing the high FD rates in the market again

Nevertheless, this time he decided to seek professional guidance before taking any action.

In his simple question, he stated that since the interest rates started rising, FDs are providing higher yields now and have become more attractive. Would it be better to redeem the portfolio and park the money back in FDs with the bank or to keep it the same way? (Read more: Best Investment Options for Doctors |All-Weather Investment Portfolio)

Because interest rates and bond prices in the economy have an inverse relationship, we explained that it was only a temporary phenomenon.

Bond prices decrease when interest rates rise, and vice versa. When the interest rate stabilizes, bond yields will rise again, thereby compensating for the recent fall in prices.

Nowadays, most Debt Mutual Funds show YTMs ranging from 6.50% to 7.50%, depending on their type.

In addition, we explained to him the benefits of debt mutual funds and bonds over FDs.

In these times, many investors have this question. Doctors generally are seen to have a skewed Portfolio. As in they may be high on Real estate or High on conservative products. In bullish times they are seen to be high on equity too. Which is not the right thing to do.(Read: Asset Allocation: The Balanced Diet to your Investment Portfolio)

FDs and Debt Mutual funds can be kept together depending on the Tax bracket you fall into. This detailed article will give you clarity on this subject.

Interest rates on FDs are rising…again :

First, let’s talk about the technical aspects.

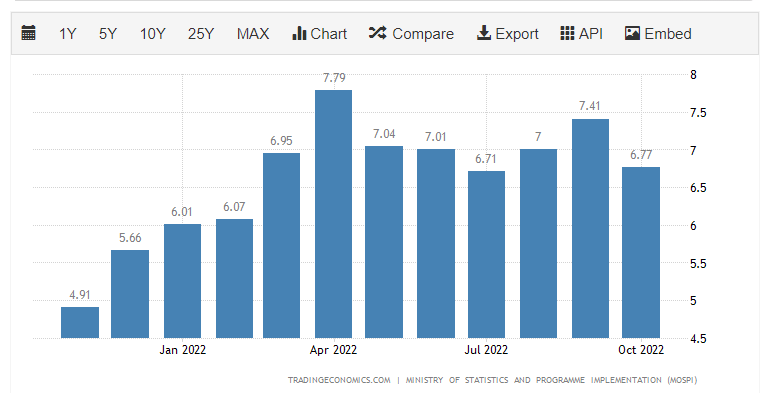

RBI has raised its repo rates over the past few months. As a result of the most recent 50 basis point hike in September2022, the repo rate is currently 5.90%, a total of 1.90% increase in the last six months.

The hike was the Fourth consecutive one in recent months. The previous hikes were 40 basis points in May 2022, 50 basis points in June 2022, and 50 basis point in Aug 2022

The RBI has been increasing the rate in order to maintain a tight grip on the rising inflation rate over the last few months, which has ranged between 6-7%. It is way above the Government’s target of 4% with the tolerance range of +/- 2%, i.e., the upper limit is 6% and the lower limit is 2%.

As a result, almost all banks have raised their FD interest rates in recent months. On 3 to 5-year FDs, large banks like SBI, ICICI, HDFC, etc. offer rates between 6.5%-7.0%. More attractive rates are offered by small banks and non-bank financial companies (NBFCs). There is an additional interest rate of 0.25%-0.5% for senior citizens.

Taxes and inflation will erode returns:

There is no doubt that FD interest rates are attractive right now, but you should take a closer look at inflation in recent months. It is somewhere between 6 and 7%, which is the upper limit of acceptable range, i.e. 6%.

In other words, the real return on FDs is negative. Because of inflation, you are losing money,as the purchasing power of the same amount is decreasing.

Dr. Raghuram Rajan (ex-RBI governor) once used a concept called “Dosanomics” to support the statement that increasing interest rates in times of high inflation yields little benefit. (Watch the video here)

The story goes like this-

An individual is fond of Dosas, and each Dosa costs Rs.50. His bank account has Rs.1 lakh. With this amount, he can purchase 2,000 dosas. He sacrifices his desire to have the Dosa now for a bank FD, believing that once the FD matures he will be able to buy more dosas.

Let’s assume the FD interest rate is 5% (Pre Tax), which means his Rs.1 lakh investment will become Rs.1.05 lakhs at the end of the year. Assuming inflation is 6% over the same tenure, the price of dosa has risen to Rs.53. Now, for the same amount, the person can only have 1,980 dosas.

As a result, investing in FDs in times of high inflation has somewhat reduced purchasing power instead of increasing it.

Taxes are another thing to consider. FD interest income is fully taxable. Therefore, if you earn 6% interest on an FD and fall under the 20% or 30% tax slab, you will net 4.80% and 4.20% post-tax. The returns are further reduced as a result.

This shows, the final real returns from FDs can be negatively impacted by high inflation and high taxes.

What alternatives are available to bank FDs?

In the fixed-income space, there are a number of low-risk alternatives to Bank FDs. Here are a few examples:

- RBI Bonds and Government securities:

- FDs of small finance banks/NBFCs:

- SCSS or PMVVY

But Considering the current Interest scenario, almost all these options fall in the same range. Though may be considered as more secure options than FDs, since Government securities and Post office deposits come with Sovereign Guarantee.

The Doctors who fall in the High Income Tax Bracket, may consider Debt Mutual funds as an alternative to the Bank FDs. Let me explain why

Debt Mutual Funds:

Though Debt Mutual funds come in different varieties, for doctors who seek a fixed certain return, a better alternative to FDs is to invest in debt mutual funds such as Fixed Maturity Plans or Target Maturity Funds. They invest in government securities and high-rated PSU bonds and hold them until maturity. So During the tenure these schemes may move up and down due to mark to market returns but on maturity are expected to generate returns equal to YTM seen at the time of investing minus expenses.

By holding them until maturity, not only are they considered safe, but the yields also become predictable.

Additionally, long-term capital gains on debt funds are tax-efficient because of indexation benefits. Debt Funds held for three years or longer would be treated as long-term gains, and gains would be calculated based on the Cost Inflation Index number. Gains on these investments are taxed at 20%.

Especially if you belong to the higher tax slabs, the tax rate becomes much lower than what you pay on FD interest.

A debt fund that is open-ended (like Dynamic bond funds or short-term funds) gives you liquidity and flexibility. Even though the return is less predictable, if you invest for a longer period of time, you will end up with a similar kind of reward.

The withdrawal of money from debt mutual funds does not incur any penalties, unlike withdrawals from FDs that Charge you in the form of low rates.

Conclusion:

While interest rates on FDs have increased after a long time, it may be a temporary measure taken by the RBI in an effort to curb inflation.

There is no doubt that FDs are useful for keeping emergency funds or funds that are needed for very near-term expenditures, especially where capital safety is of primary concern. The drawback is that they are not efficient if you have an investment duration of more than three years.

In the fixed income space, there are other efficient alternatives that offer better yields and are comparatively safer. Doctors should consider Debt Mutual Funds for this purpose.

{kind=link}