A mistake is an error or an incorrect action or decision that is made unintentionally. It means that something was not done as intended or as expected and can result in negative consequences.

Sometimes if the Results are not negative, that may not mean that the action in the beginning was not a mistake. For e.g. If the health of a smoker never goes down, that does not mean smoking is not bad.

Mistakes happen because of a variety of reasons such as lack of information, lack of experience, incorrect assumptions, miscommunication, emotional impulsiveness, and more.

However, these days the information flow is so huge and fast, that mistakes happen when you construe the noise around as knowledge. This results in Overconfidence of knowing the subject you know hardly about, based on which you tend to make many investment and life decisions.

This is what Social media is doing these days.

Doctors are not Expected to make Mistakes. At least not in their profession, something which impacts their Patients, as any misjudgement may prove costly to health and sometimes life of the patient. So professional vigilance is a must for the Doctors.

FREE Download

YOUR FINANCIAL DATA

RECORD KEEPER

Organize and Collate data at a Single Place for easy Access and Management

And when it comes to Investment management, due to the busy schedule, Doctors may have limited time to research and manage their investments, leading to a lack of attention and discipline in their investment strategy.

At the end they tend to rely on the Bankers, Product Agents or even Family members for advice on the personal finance matters.

Investment Mistakes by Doctors

Below, I have listed down 5 Investment mistakes which many doctors make when they do not follow a structured investment strategy based on their goals. Thus should be cautious about

- Skewed Portfolio:

Lack of time and Busy schedule, results in accumulation of money in the savings account of doctors. Salary comes and Stays there for a long time.

When you find time to look into the accounts, you either switch the money to Fixed deposits or go for a Big Purchase like Real estate.

Sometimes you get a sales pitch from the Bankers where you have the account, on the “Great Investment Product, with Guaranteed Returns”, and you get sold to the same and start paying heavy Insurance premiums.

All this will lead to a skewed portfolio, which has no structure behind and result in accumulation of ill liquid investment products not suitable to your goals.

Too much of anything is bad. You have to have a Properly allocated and diversified Investments, after understanding the aspects like Risk, Liquidity and Growth, and have a goal based portfolio in place.

Remember it’s not about you only but for your family, and thus you should invest in products which are expected to be managed well by the family too. (Read: How should doctors plan their First Home Purchase?) - Heavy Loans

Loans are not difficult to get for Doctors. And even doctors are confident in their repaying capacity so they do not shy away from taking loans. (Read: How doctors should plan their borrowing?)

You may be serving education loans before actually starting working, and later get yourself into Vehicle Loan, Personal Loan…and then Home Loan, Practice loan etc.

Even Lender does not mind loaning doctors, but still they prefer to maintain the financial hygiene and may stop when the EMIs equals 50% of the Income. But this is Bank’s Financial Prudence, not the borrowers’.

If doctors do not follow the financial discipline they will get into a stressful debt cycle, where the cash flow positions will get compromised. To cover up the EMIs, to make more money, you will have to work harder, which may take a toll on your health and result in other problems. (Read: Should you Consider Prepaying of loans?)

We call it the management of Lipid profiles in personal finances. Doctors should be aware of the same, and not to go overboard on borrowing. - Starting Late

Due to late start in Working / Earning Life, mostly in the late 20s, and then spending next 5-10 years gaining experience and expertise and doing super specialization, doctors tend to compromise on most of the early stage money compounding benefits.

Though this is also true that after all these years, the Doctors’ Income also gets a decent push and increases manifold, but along with the other responsibilities and Lifestyle expenses too. And if you have loans to serve, then the Savings potential takes a hit. (Read: Financial Planning Tips for Young Doctors)

So it is wise to start saving the moment you get your first paycheck. And if you think you have lost the bus, it’s never too late. Have a Plan at place and see how much you can save more for your goals, and take action.

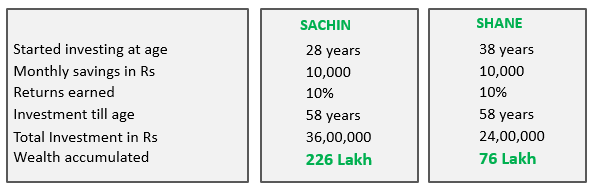

Cost of Delay

You can see from the above table that the Investment difference is just 12 lakh, but that resulted into Rs 150 lakh of wealth difference, with 10 years delay. Now if Shane wants to catch up with Sachin, he has 2 choices: Earn 18% or increase the savings to Rs. 30000.

Increasing savings may not look like an issue with the rise in income over 10 years , but remember, the income potential of Sachin will also increase, and he can multiply the money faster than Shane.

It’s not about who makes what, but showing you the benefits of early start. - Self medication

Yes. Even Doctors have this problem. Though it is fine on the medical side since they have the knowledge, but on Financial side they need to be cautious enough to follow the “Self-Investment” route.

If not self, but taking advice on medicines from chemists is also not advisable. So, why do you consider Bankers, Product Agents , Insurance sellers, or even family members for that matter for the Financial Advice.

Please understand that Sellers will sell what they want to sell, not what you need or is good for you. Whereas like doctors, an Advisor will never advise without proper diagnosis. (Read: How doctors should chose Financial Advisors in India?)

You may not be aware of the fact that there are Certified and Regulated Professionals Present in the market, who have fiduciary responsibility to advise the Clients well on their Financial Management.

It’s just, you have to take interest and Initiative in your financial well being and then only you will be able to find the advisor suitable to you. (Read: How and When Doctors behave like their patients?) - Misunderstanding Risk

Risk in whatever way you understand it, is the possibility of loss or damage, as well as the uncertainty associated with potential positive or negative outcomes.

You must agree, there is a risk in taking medicines and also in not taking medicines.

Same way even if you are Scared of Financial markets, risk is in not investing too.

The chances of negative impact reduces when you take medicine under a professional guidance, same way when you follow a financial plan designed by SEBI Registered Adviser, the risk of getting into wrong investments is reduced significantly.

It’s all about understanding. Safety has its own risk. No “safe instrument” can beat Inflation over a longer run. But still safe instruments can not be ignored in a portfolio for shorter duration goals or for emergency funding.

I have seen doctors who never like to invest in Equity markets calling it volatile and unsafe, are heavily invested into Real estate, Considering it as a safe investment. (Read: Why Real Estate is Considered as Riskier to Equity?)

Also, some doctors who used to invest in Cryptos (saying they like taking risk) suddenly these days are seen only in FDs (these are 2 extremes)

Your Greed and Fear should never guide your Investment decisions. There has to be a Strategy at place, based on your risk tolerance and goals targeted. (Read: Financial Goals of doctors at different Life stages)

Conclusion:

Mistakes are an inherent part of the human experience and serve as opportunities for learning and growth. By recognizing and acknowledging mistakes, individuals can reflect on what went wrong and make necessary changes to improve their behavior or decision-making in the future. This is why mistakes are often seen as an important part of the learning and development process.

However, some mistakes are proved to be a lot more costly and some, rather than making you wise, put you on a risk averse mode. These should not be the preferable outcomes, which is where it is important for doctors to understand their challenges, Limitations and aspirations and work towards all round growth and focus on the things matters to them most by delegating the work which is not their domain to the experts to reduce the mistakes, including the investment mistakes and improve well being

Remember, even professionals make mistakes, but they also know how to correct them.

Be Good with your Money!

Subscribe our Wealth Care Newsletter and get one PREMIUM ARTICLE PER WEEK on your Personal Financial wellness, directly in your Inbox.

{kind=link}